What is a Target Date Fund? is a common question among novice investors. A target date fund holds stock and bond index funds and rebalances the relative weight of each asset class over time such that you will start out owning more stocks when you are younger and end up owning more bonds when you are older.

As the allocation between stocks and bonds changes automatically over time, the benefit for you is that you won’t have to think about asset allocation over time. The target date fund will automatically adjust for you as you age.

Target date funds are typically named with the year the owner of such fund is expected to retire. For example, a Target Date Fund 2060 presumes that you will retire in 2060.

Right now, a Target Date Fund 2060 will contain more stocks than bonds on the theory that you have time on your side to take on more risk.

As we get closer to the year 2060, the target date fund will adjust such that ultimately you’ll own more bonds than stocks on the theory that you will be needing the money soon and so cannot afford to take on the risk of stocks.

Who should buy target date funds?

As you long as you purchase low fee target date funds, these are perfect investments for a novice investor. Early in your investing career, the most important thing to do is to get started.

Target date retirement funds let you “set it and forget it” while you focus on building up your investing accounts.

Advanced investors will complain that target date funds often contain unnecessary fees because they are essentially a “meta fund” where you’ll be responsible for paying the fees for all of the underlying mutual funds.

This may be true but there are many extremely low fee mutual funds (see below for some examples).

Regardless, early in your investing career it’s better to focus on your savings rate than minimizing fees.

Paying _slightly_ higher fees for the first five years of your career is not going to prevent you from becoming wealthy. Waiting five years to begin investing is going to cause problems.

Once your account grows to large amount (e.g. $100,000?) you can re-examine whether it makes sense to switch out of the Target Retirement Fund into your own asset allocation.

How do target date funds work?

You can think of Target Date Funds as “meta funds” which hold multiple asset classes.

A typical Target Date Fund will contain separate funds each representing a target asset class such as:

- Total US Equity Market

- Total Non-US Equity Market

- Total US Bond Market

- Total Non-US Bond Market

If you invest in those four asset classes, you’ve effectively invested in the world’s entire equity and bond market.

The Target Date Fund selects an allocation between those four asset classes that is appropriate for your age.

As you get older, the administrator of the Target Date Fund will slowly adjust the asset allocation between those four asset classes.

Meaning the equity funds will decrease over time and the bond portion will increase.

By offloading risk and increasing the amount of bonds you own, you should expect less volatility and lower returns.

That may not sound good but as you get closer to retirement, you want lower volatility and lower returns to ensure that you don’t end up with significantly less money than you thought once you retire.

What are the best target date funds?

Nearly all of the big mutual fund companies offer Target Date Funds.

That means you can expect to find them at places like:

- Vanguard (Target Retirement Funds)

- Schwab (Target Funds)

- Fidelity (Freedom Funds)

- TIAA-Cref (LifeCycle Funds)

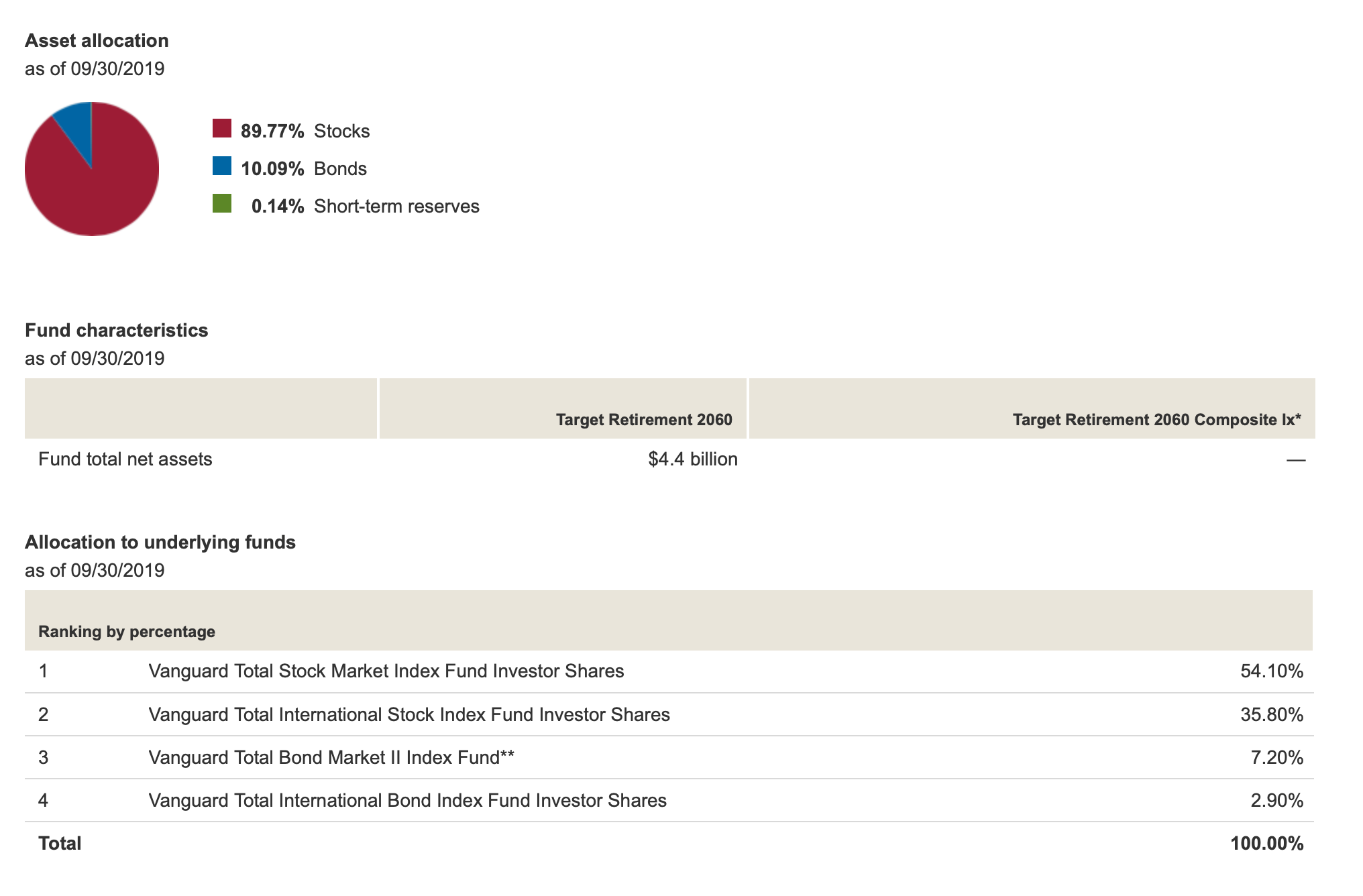

Vanguard target retirement fund 2060 (VTTSX)

Let’s look at the Vanguard Target Retirement Fund 2060 (VTTSX).

For a lawyer looking to retire in 2060, Vanguard proposes an asset allocation of approximately 90% stocks and 10% bonds (of which the equity is split 60/40 between the United States and International stock markets and the bonds are split 70/30 between the United States and International bond markets).

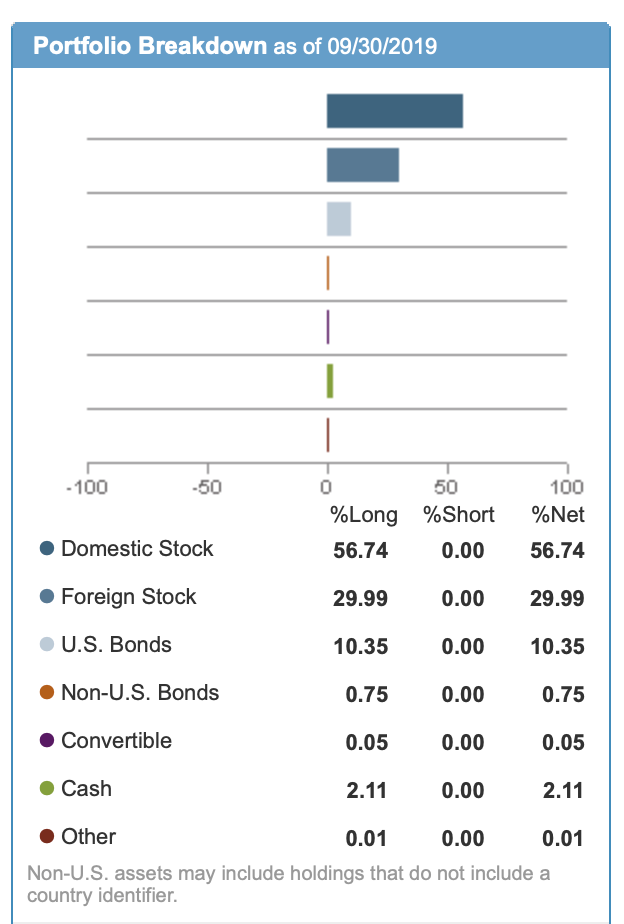

Schwab target 2050 index fund (SWYHX)

Here’s a breakdown of Schwab Target 2045 Index Fund (SWYHX).

Schwab is proposing that a lawyer who wants to retire in 2045 should have a little more than 85% in stocks with the balance in bonds and cash.

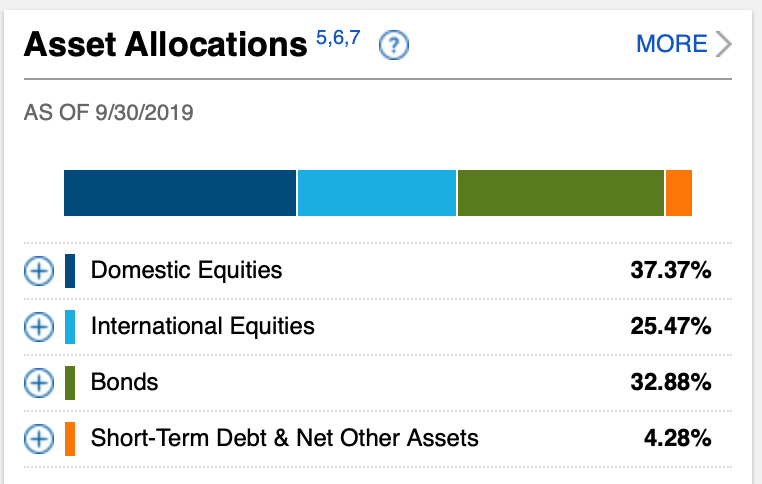

Fidelity freedom 2025 fund (FFTWX)

Here’s a breakdown of Fidelity Freedom 2025 Fund (FFTWX), which is geared toward an investor who expects to retire in the near future.

As you can see, the asset allocation is completely different.

The Fidelity Freedom 2025 Fund has closer to 60% of the total fund invested in equities and the remaining 40% in bonds and cash.

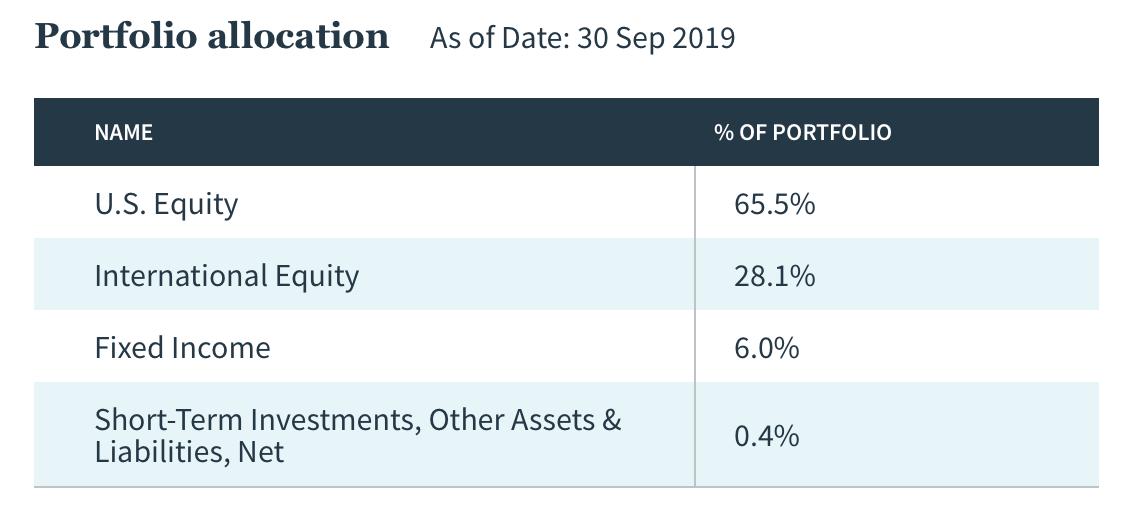

TIAA-Cref lifecycle index 2060 fund (TVIIX)

Here’s a breakdown of TIAA-Cref Lifecycle Index 2060 Fund (TVIIX).

As we would expect, TIAA-Cref has a more aggressive allocation of nearly 95% in stocks and 5% in bonds given the time horizon.

What fees are associated with target date retirement funds?

Earlier, we talked about Target Date Funds from four of the larger mutual funds companies.

Now, let’s take a look at the fees for each fund. These are the four we explored above:

- Vanguard Target Retirement Fund 2060 (VTTSX)

- Schwab Target 2050 Index Fund (SWYHX)

- Fidelity Freedom 2025 Fund (FFTWX)

- TIAA-Cref Lifecycle Index 2060 Fund (TVIIX)

And here’s those same four Target Date Funds with their annual expense ratio.

- Vanguard Target Retirement Fund 2060 (VTTSX) – 0.15%

- Schwab Target 2050 Index Fund (SWYHX) – 0.08%

- Fidelity Freedom 2025 Fund (FFTWX) – 0.65%

- TIAA-Cref Lifecycle Index 2060 Fund (TVIIX) – 0.10%

What does the expense ratio tells us?

It means that for every $1,000 you have invested, you will pay $1,000 × the expense ratio in fees each year.

For example, Vanguard is charging $1.50 per year per $1,000 in management fees.

If you have $40,000 in the Vanguard fund, you’ll pay $60 a year for them to manage it.

If I were just making a decision on fees, I’d prefer the Schwab Target Date Fund since it charges the lowest fee.

But honestly, all of the fees are fairly low.

Fidelity is the most expensive and you’d still only be paying $260 a year if you had $40,000 invested with them.

Remember that when you’re getting started, your savings rate is way more important than than your investment return or a minor difference in fees.

Focus on piling up as much money as you can today.

And then you can focus on optimizing a portfolio once you have a big balance tomorrow.

Joshua Holt is a former private equity M&A lawyer and the creator of Biglaw Investor. Josh couldn’t find a place where lawyers were talking about money, so he created it himself. He spends 10 minutes a month on Empower keeping track of his money. He’s also maxing out tax-advantaged accounts like 529 Plans to minimize his taxable income.